8 observations from IMN Asset Management 2025

At the 2025 IMN Real Estate Asset Management conference, Pereview’s VP of Client Success Ron Rossi led a candid discussion on how firms are navigating one of the toughest decision points in commercial real estate: when to hold, when to sell, and when to buy.

Joined by panelists Brandon Cohen from Harbert Management Corporation, Mario Kilifarski from Fundamental Asset Management, and Max Rodenborn from Zenith IOS, the conversation centered on how managers are adapting strategies amid rising costs, shifting investor expectations, and growing pressure to deliver liquidity in a volatile market.

What emerged was a clear snapshot of the current state of play: cautious, data-driven, and uneven across asset classes and fund structures.

1. Market sentiment is divided, but active

Around the room, the consensus was clear: There is no real consensus.

Some asset managers are pressing pause, waiting for rate clarity and pricing stability before making moves. Others are leaning into the uncertainty, actively deploying capital into distressed or non-core assets that offer upside once conditions normalize.

As a result, business plans are changing rapidly, underscoring the importance of centralized, standardized data for strong visibility into assets and portfolios.

2. Fund structure drives behavior

With many firms managing closed-end vehicles, hold-sell timing is often dictated by fund maturity.

- Older vintages are in harvest mode, seeking liquidity in a tough market for distributions

- Newer funds are still creating value and opportunistically deploying capital

Panelists emphasized the need to balance investor expectations for distributions with today’s limited exit liquidity and lender inflexibility around extensions and rate caps.

Fund maturity dates and loan extensions are shaping strategy. Some assets have to be sold, while others can be held and restructured, depending on lender flexibility and fund mandates. Where you are in the fund life helps dictate whether you may be looking to sell or not.

3. Decisions rely on performance data

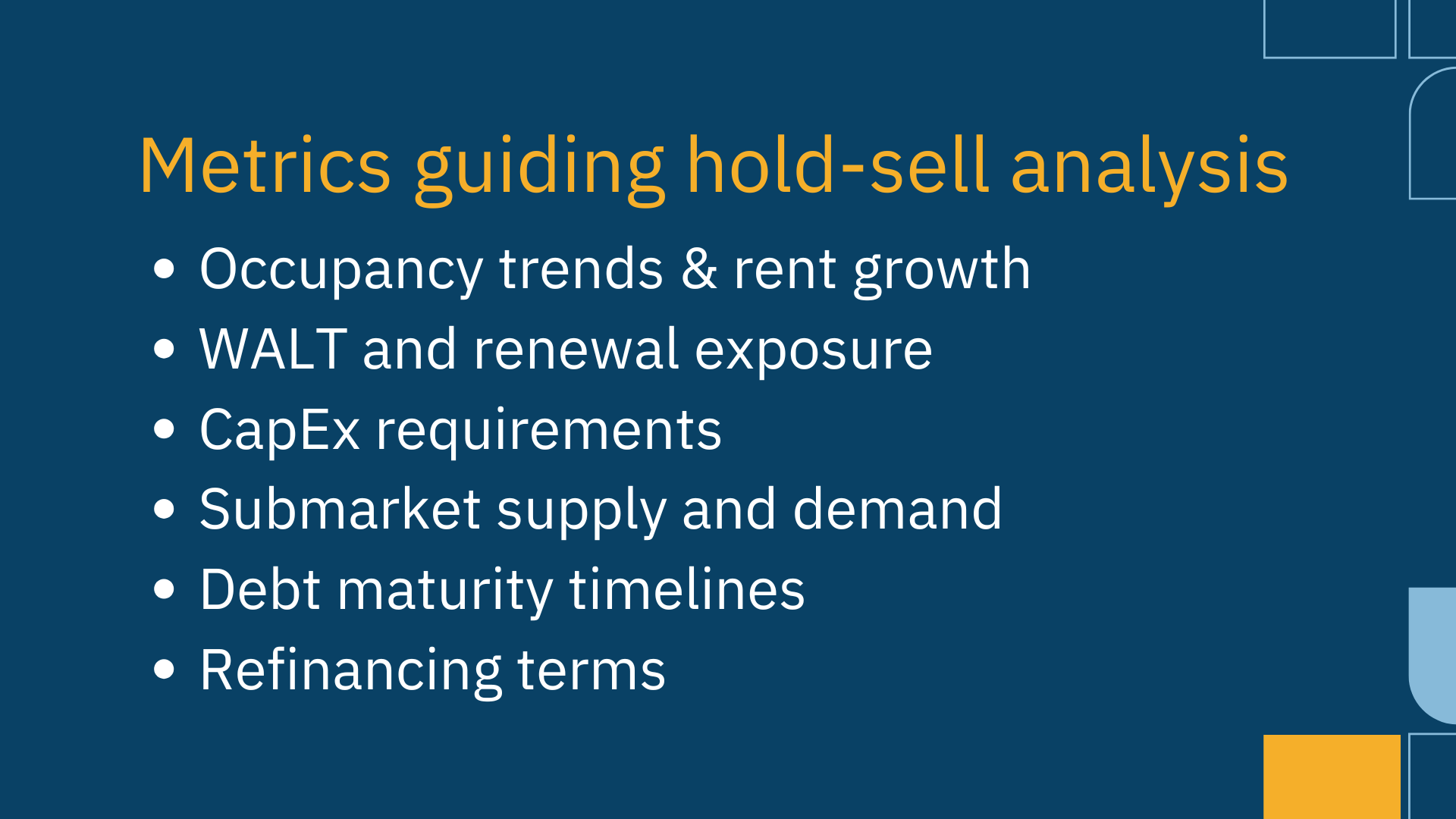

When asked what metrics guide hold-sell analysis, panelists cited a consistent list:

- Occupancy trends and rent growth

- Weighted average lease term (WALT) and renewal exposure

- CapEx requirements

- Submarket supply and demand

- Debt maturity timelines and refinancing terms

One panelist framed it simply: “Have we created the value we expected – and if we sell now, can we reinvest that capital at a higher return?”

This redeployment mindset underscores the importance of reliable data. Asset managers need the ability to model multiple exit scenarios quickly and confidently – which is why so many rely on systems like Pereview to aggregate, standardize, and visualize these scenarios at the fund and portfolio level.

4. Market conditions vary by sector and region

The panel agreed that macro-level generalizations don’t tell the full story.

In multifamily, oversupply in the Sunbelt – particularly in Dallas and Texas metros – is creating downward rent pressure, forcing owners to reduce rents by up to 20–25% to maintain occupancy.

By contrast, industrial outdoor storage (IOS) remains a bright spot, with growing institutional investment and tenant demand. “It’s a space that’s institutionalizing,” said Rodenborn. “Tracking who’s entering the market and when capital is flowing helps us time our exits.”

Several firms are also diversifying into niche or special purpose properties, from transportation assets to specialized operating businesses, to offset traditional CRE headwinds.

5. Valuations are stabilizing, but not yet firm

Broker Opinions of Value (BOVs) remain the most relied-on pricing benchmarks, though final sale prices often land 4 to 5% below those numbers, which is a reflection of limited buyer pools and extended transaction timelines.

Fewer bidders and longer timelines have replaced the multiple-offer bidding wars of prior years, and lenders still prioritize stamped appraisals over market-informed opinions.

At the same time, lenders continue to prefer certified appraisals over broker-driven market insights, often creating friction between valuations and financing expectations.

6. Investor expectations are shifting

Several panelists described what they called a “distribution drought” – the challenge of managing investor relationships during extended hold periods and delayed exits.

This makes transparency important. Regular communication through quarterly letters and investor calls is critical, especially when distributions are lower than anticipated.

Many firms are supplementing investor updates with case studies and portfolio-level analysis, showing how strategic decisions – such as refinancing or temporary cash-in strategies – preserve long-term value even when short-term liquidity is limited.

7. Technology remains both indispensable and imperfect

When the conversation turned to tools, the answers were unanimous: Argus and Excel still rule the modeling world, often supplemented by other platforms like Red IQ, Salesforce, and MRI.

But even the best models have limits. “The second we hit save on a model, it’s already wrong,” Kilifarski joked, reminding everyone how quickly assumptions can change.

That volatility is precisely why firms are investing in platforms like Pereview, which provide a single source of truth across all assets, funds, and positions in the capital stack. By consolidating financial, operational, and loan data into one environment, asset managers can make faster, more confident decisions – and adapt models as market conditions shift.

8. Debt pressures are reshaping collaboration across the capital stack

Panelists noted that today’s market is testing the relationships between equity, debt, and operating partners. Loan maturities, tighter credit, and stricter underwriting standards are forcing firms to get creative – from cash-in refinances to short-term extensions and debt acquisitions.

These dynamics are blurring the traditional boundaries of the capital stack, requiring greater collaboration between lenders, operators, and investors.

For firms with strong data visibility and lender relationships, the same environment that limits liquidity can also unlock opportunity: acquiring assets or debt positions from overleveraged owners at favorable terms.

The consensus? Those with disciplined underwriting, diversified portfolios, and clean, connected data will emerge stronger from this cycle.

The bottom line

In this volatile market, the primary differentiator is data clarity.

Whether holding, selling, or buying, firms that can trust their data – and act quickly on it – are best positioned to protect investor returns and capture emerging opportunities.

As the hold-sell panel discussion underscored, the next wave of competitive advantage in real estate asset management won’t come from predicting the market. It will come from seeing it clearly.