CRE’s “tale of two debt markets” is unfolding – and data visibility will decide who benefits.

According to Deloitte’s 2026 Commercial Real Estate Outlook, the debt markets are splitting in two.

On one side, legacy loans – many originated in 2021–2022 – are straining under higher-for-longer rates, tight spreads, and maturing debt-service coverage requirements. Over half of global CRE leaders surveyed said they have property loans coming due this year.

On the other side, new origination is accelerating. With property values stabilizing and lenders returning to the market, the first half of 2025 saw a 13% increase in new loan volume and tighter spreads.

This brings us to an “old risk, new opportunity” moment.

The firms that outperform in 2026 won’t just survive their refinancing calendar – they’ll leverage it. y.

What some call risk, Pereview turns into visibility

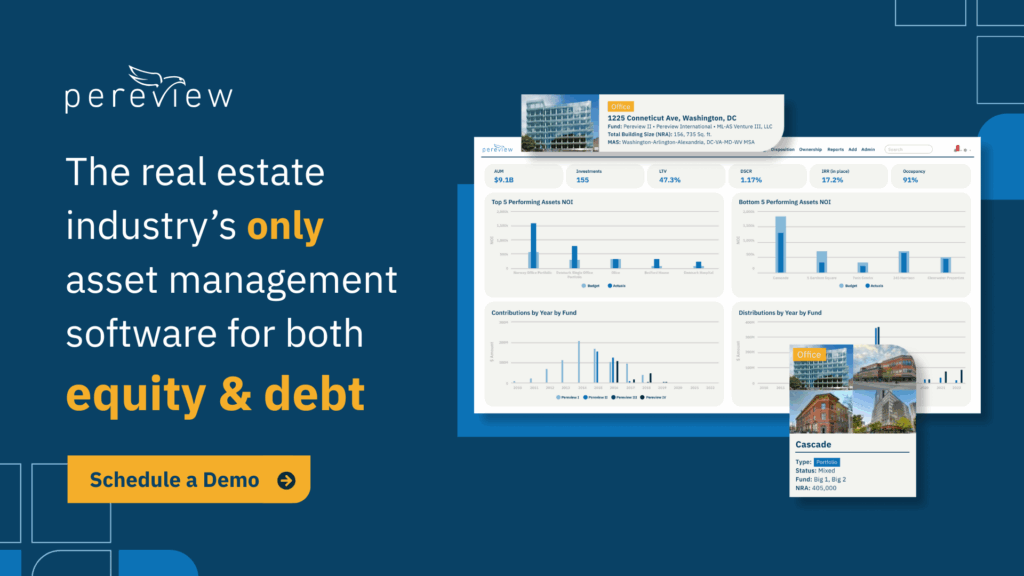

The biggest challenge in navigating today’s debt markets isn’t rate volatility – it’s data fragmentation. Loan data often lives in PDFs, shared drives, or lender portals, disconnected from asset and fund performance metrics.

Without a single source of truth, it’s nearly impossible to:

- Track upcoming maturities and covenants across portfolios

- Compare loan terms or stress-test coverage ratios

- Understand debt’s impact on fund- or asset-level returns

- Present lenders with consistent, transparent reporting

That’s where Pereview’s debt as an asset framework comes in.

Managing debt as an asset, not a liability

Pereview unifies loan, asset, and fund data into one system, enabling teams to analyze, report, and strategize from the same dataset – whether they’re refinancing, restructuring, or acquiring new debt.

Here’s how it works:

1. Centralize every loan record

- Capture loan-level terms, maturity dates, and amortization schedules.

- Link each loan directly to its asset and fund.

- Store lender contacts, rate details, covenants, and draw schedules.

2. Automate document ingestion

- AI extracts key terms from loan agreements and amendments in minutes.

- Standardized fields populate automatically for reporting and validation.

3. Visualize exposure and risk

- Pereview’s Loan Maturity Dashboard displays every loan by date, rate type, and risk status.

- DSCR heatmaps highlight coverage issues before they trigger default.

4. Streamline lender communication

- Generate lender-ready covenant reports with audit trails.

- Track loan compliance workflows – variance reviews, waivers, and renewals – in one place.

5. Connect debt and equity views

- Understand capital stack performance at every level.

- Compare debt cost and equity yield side-by-side across funds or portfolios.

With Pereview, the loan isn’t just a risk – it’s a dataset that drives better decisions.

From “extend and pretend” to proactive planning

Deloitte noted that many lenders and borrowers have relied on short-term extensions to delay difficult refinancing decisions. But the firms leading the next cycle will use data to get ahead of the maturity wall, not wait for it.

With Pereview, firms can:

- Scenario-test refinancing options – private credit, bank debt, or CMBS – based on current property performance.

- Model cash-flow impacts of new rate structures or partial paydowns using connected Excel models.

- Identify properties most at risk for covenant breaches or liquidity gaps and plan mitigation early.

That’s not just portfolio management – it’s risk prevention through real-time intelligence.

New lenders, new data requirements

Deloitte’s outlook also highlighted the growing role of private credit funds and nontraditional lenders, which now account for nearly a quarter of U.S. CRE loan volume. These lenders bring flexible capital – but also demand higher transparency and faster data delivery.

With Pereview’s standardized data model and automated report generation, you can deliver detailed, audit-ready packages to any lender, in any format, without building new templates each time.

As traditional banks cautiously re-enter the market, that same transparency can mean tighter spreads, faster closings, and improved lender confidence.

Turning refinancing risk into portfolio strategy

By managing both legacy loan risk and new debt opportunity within the same platform, Pereview clients gain:

- Complete debt visibility – all maturities, rates, and covenants in one dashboard

- Reduced refinancing risk – automated alerts for DSCR and LTV thresholds

- Higher data confidence – AI-driven validation across source systems

- Faster decision cycles – connected Excel models and Power BI analytics

- Smarter capital allocation – clear view of debt cost vs. asset returns

The takeaway

Deloitte’s 2026 report says CRE lending is coming back – but only for firms that can demonstrate strong data discipline, accurate reporting, and transparent risk management.

That’s exactly where Pereview delivers.

By unifying loan, asset, and fund data into one source of truth, you can stop managing debt in spreadsheets and start managing it as an asset.